Submitted by TAC Benefits Group

What is the status quo? It usually goes something like this. Your broker delivers a renewal from your current commercial carrier. The renewal is typically delivered 60 days prior to renewal and is around a 23% increase in premium from your prior year. Your broker promises you a market search for a better price. After going to the market, they come back with 2 quotes, 3 declined to quote, and some alternatives being offered by the current carrier. They negotiate with the carriers and come back with a 12% increase if you switch carriers (disruption), and you increase your deductibles and copayments. You accept this position in the final weeks before renewal and move on hoping next year will be better. Next year you repeat the same exercise, because it has to get better at some point, right? Wrong!!!

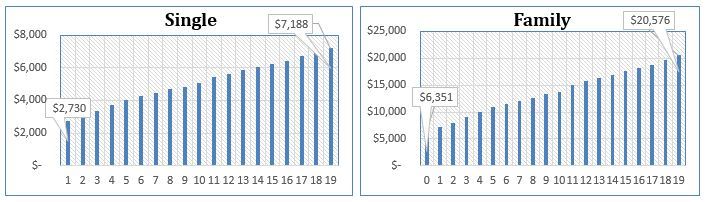

Health insurance premiums have increased by 0ver 200% since the year 2000. Employer contributions have increased just under 200%, and employee contributions have increased around 250% in the same time period. This is clear evidence that “the status quo must go”.

*Data provided by The Kaiser Family Foundation Benefits Survey 2000-2019.

Many employers, including those with under 100 employees, have resorted to utilizing self-funded programs to control their cost through increased transparency. In 2019, 35% of small employers (defined as 3 to 199 covered employees by KFF) are now in self-funded plans, as compared to less than 20% in the year 2000. This is a trend that industry experts expect to continue to grow, so much so that some states are fighting back against small group self-funded health plans, specifically New Jersey. You might ask why the state would want to eliminate programs that help small employers reduce their health insurance cost. The answer is simple, special interests and taxes. You should consult with your broker or advisor to see if self-funded programs would be beneficial to you as an employer.

How does a self-funded plan help a small employer to control the costs? Isn’t self-funded too risky for a small employer? Self-funded plans provide complete transparency as to how your healthcare spend is being utilized. This transparency helps your broker negotiate with the underwriter based on your utilization, and allows your TPA/Broker to use your data to promote cost saving programs specific to your spend. Small group self-funded programs have been designed to eliminate the risk typically associated with self-funded plans through proper placement of stop loss insurance.

Since the mid-1980s employers have been told that the best way to lower costs is to utilize a carriers PPO network to receive deep discounts on billed charges from healthcare providers. It is true that carriers such as Blue Cross, United Health Care, Cigna, Aetna, Amerihealth, and Oscar can offer discounts as high as 60% off of billed charges. However, there is no federal or state legislation on the books, or even being considered, to regulate billed charges. Each hospital and facility have their own unique chargemaster. These chargemasters can differ considerably for procedures performed by the facility.

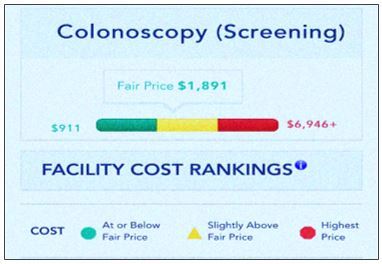

The below illustration provided by Healthcare Blue Book emphasizes the significant difference in pricing between facilities situated in close geographic proximity.

** Data provided by Healthcare Blue Book

As illustrated the same procedure for a colonoscopy screening can differ by as much as 800% from one facility to another. Price transparency is another way to control health care spending in your plan.

Besides transparency and properly placed stop loss insurance, what else can I, as an employer, do to reduce my benefits costs? Referenced Based Pricing (RBP). RBP is a data-based reimbursement tool, resulting in employer savings of 20% to 30%.

RBP eliminates the commercial carriers’ capacity to protect their most valued asset, their providers, via their high cost PPO arrangements, and place the focus back on the patient.

What is Referenced Based Pricing and how does it save me money? RBP is a healthcare cost containment model that limits what a group health plan will pay for certain high-cost services including hospital and outpatient facility charges. There are a variety of reference-based pricing strategies employers can implement. Most often, the reimbursement rate is 120 percent to 200 percent of Medicare for a given service, based on what's reasonable in terms of the local health care market.

The key to implementing a referenced based plan, is employer buy-in and understanding of the product. Employers should take some time to understand the concept of RBP, which will result in significant savings on their benefit spend. Implementation of RBP requires strong communication to the employees, which should be created by your broker. Your broker should do employee meetings whenever possible to educate employees and provide them with the tools they need to navigate the program.

Michael Cleary and his team at TAC Benefits Group will be presenting on Referenced based pricing and healthcare pricing transparency at the NJSA Law Conference on February 13, 2020.

Click here to download the article in PDF format.